Spotify Stock Slips Following U.S. Price Increases — Some Investors Anticipated Larger Bumps, Citi’s Jason Bazinet Notes

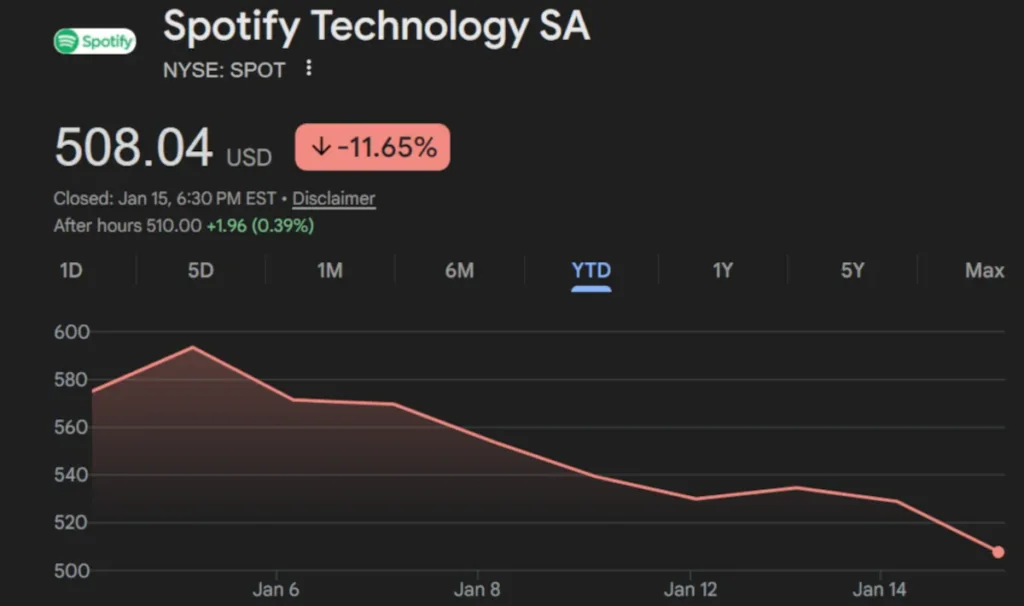

At least for now, Wall Street doesn’t seem enthusiastic about Spotify’s latest U.S. price increases. During today’s trading, the company’s stock (NYSE: SPOT) parted with 4% of its value and, in the process, reduced its year-over-year growth to 3.5%.

We broke down those stateside price bumps (plus adjustments in Estonia and Latvia) soon after their announcement this morning. In short, the raises mean Student ($6.99 per month), Individual ($12.99), Duo ($18.99), and Family ($21.99) alike cost more in the States.

Naturally, the new monthly charges are presenting questions about Spotify’s subscriber outlook and potential churn – especially given the comparative affordability of rivals like Apple Music and Amazon Music.

But in general, the major labels, a number of analysts, and others have long been calling for continued increases. Following that fact to its logical conclusion, higher monthly charges in the world’s largest economy should be music to investors’ ears.

As initially highlighted, this presumed approval hasn’t yet translated into a share-price improvement. SPOT finished the day at $508, up materially from a couple years ago but down roughly 12% across the past two weeks alone.

Of course, there’s plenty of room to speculate about what the slip means. Has the company pushed the pricing envelope too far? Will the increases compel pivots to Spotify Free and bring the company’s advertising challenges back into the spotlight? And if the answer to either is yes, what does it mean for the timing of future raises?

However, with the company’s first post-increase-implementation earnings report not scheduled to arrive until well into 2026, said speculation isn’t very helpful in the near term. On the other hand, it’s certainly worth exploring the growing pile of SPOT target reductions.

On the heels of Goldman’s Spotify stock target recalibration last year, Wells Fargo, Bernstein, Oppenheimer, UBS, Cantor Fitzgerald, and Guggenheim just recently sliced their own targets, we reported yesterday.

Towards the lower end of the forecasts, Cantor Fitzgerald predicted a journey to $615 for SPOT; it doesn’t really need saying that the general downward trend isn’t exactly encouraging for investors.

Nevertheless, SPOT’s climbing back to $615 would still represent a huge rebound, and different (reduced) targets are implying even bigger boosts than that. Jefferies today predicted that Spotify stock would return to $750 per share, for instance, while UBS previously expressed the belief that SPOT would crack a record high of $800.

Explaining the outlook, Jefferies mentioned possible revenue jumps stemming from superfan offerings and AI upgrades, besides reiterating Spotify’s global subscriber-growth momentum.

Elaborating on his own view, including a $650 target, Citi’s Jason Bazinet noted that some analysts had been anticipating a $2 Individual price increase. Looking beyond dollar signs to market realities, we can see that it probably wouldn’t be wise for Spotify to charge $36 more per year than Apple Music.

Link to the source article – https://www.digitalmusicnews.com/2026/01/15/spotify-stock-slip-price-increases/

-

Squier by Fender Precision Bass Guitar Kit, Affinity Series, Laurel Fingerboard, 3-Color Sunburst, Poplar Body, with Guitar Bag and Rumble 15 Amp Bass Amp, Cable, Guitar Strap and More$379,99 Buy product

Squier by Fender Precision Bass Guitar Kit, Affinity Series, Laurel Fingerboard, 3-Color Sunburst, Poplar Body, with Guitar Bag and Rumble 15 Amp Bass Amp, Cable, Guitar Strap and More$379,99 Buy product -

Alesis Recital Grand – Digital Piano 88 Weighted Keys with Hammer Action, Sustain Pedal, 16 Premium Voices, Speakers, Piano Lessons, Sheet Music Stand$449,00 Buy product

-

Music Treasures Co. Banjo Miniature$16,79 Buy product

-

John Packer JP176 Eb Soprano Cornet$0,00 Buy product

-

GLARRY Electric Bass Guitar Full Size 4 String Exquisite Stylish Bass with Power Line, Bag and Wrench Tool (Red)$119,95 Buy product

-

Clucker-Truss Elastic Gourmet Trussing Strings; 5 Inch BLUE; Bulk bag of 3,750 Ties (250 Bundles of 15/Bundle)$167,99 Buy product

Responses